Key Points

- AI-driven FinCrime detection strengthens fraud prevention by identifying real risk more accurately and reducing unnecessary alerts.

- Machine learning reduces false positives through behavioral analysis, predictive models, and smarter alert prioritization.

- KYC automation improves alert quality at the source by ensuring accurate identity data and continuously updated customer risk profiles.

- AI enables faster, risk-based decisions that improve compliance efficiency while minimizing customer friction.

Sophisticated Threats, Urgent Decisions

Financial crime has entered a new era. Fraud, money laundering, cybercrime, and identity abuse no longer operate in isolation. They converge across channels, customer journeys, and geographies, overwhelming traditional detection systems and compliance teams.

Consumer fraud losses exceeded $10 billion in 2023 in the US, nearly doubling in just three years¹. In parallel, UK Finance reports continued growth in authorized push payment fraud and identity-driven scams across faster payments². At a global level, regulators and industry bodies now recognize that fraud and AML risks are deeply interconnected³.

Banks, fintechs, credit unions, and payment companies are not lacking detection tools. Most institutions already run sophisticated transaction monitoring engines and fraud rules. The real issue is different and far more urgent.

Alert volumes are exploding. False positives are draining operations. Customer experience is deteriorating. And regulators expect a unified, explainable view of risk.

AI-driven FinCrime detection, supported by strong fraud prevention strategies and intelligent KYC automation, has become a strategic imperative.

What Is AI-Driven FinCrime Detection?

AI-driven FinCrime detection applies machine learning, advanced analytics, and behavioral intelligence to identify suspicious activity across fraud, AML, and customer risk in real time.

Unlike static, rule-based systems, AI models analyze large volumes of structured and unstructured data to distinguish legitimate behavior from fraud with greater precision. Research from McKinsey shows that machine learning models can reduce false positives by 20 to 50% compared to traditional rules engines when properly implemented⁴.

Modern AI-driven detection spans the full risk lifecycle:

- Digital onboarding and identity verification

- Transaction and payment monitoring

- Fraud and AML investigations

- Regulatory reporting and SAR preparation

When combined with KYC automation, AI enables institutions to reduce friction for low-risk customers while concentrating human expertise where risk is highest.

How AI Improves Fraud Prevention

Pattern Recognition and Predictive Analytics

AI models learn from historical transaction data, customer behavior, and known fraud typologies to identify subtle indicators of risk. These include behavioral changes, transaction sequencing, device inconsistencies, and velocity shifts.

According to the Bank for International Settlements, behavioral analytics and predictive modeling are now central to effective fraud prevention in real-time payment environments⁵.

Supervised and Unsupervised Learning

Effective FinCrime programs combine multiple learning approaches:

- Supervised learning, trained on labeled fraud and non-fraud cases, detects known threats such as account takeover or synthetic identity fraud.

- Unsupervised learning identifies anomalies without predefined labels, enabling detection of new or evolving fraud patterns.

This dual approach allows institutions to adapt faster than criminals, who constantly modify tactics to bypass static rules.

Core AI Capabilities Powering Modern Fraud Prevention

Real-Time Transaction Monitoring

AI enables near-instant analysis of transactions across payment rails such as ACH, FedNow, Faster Payments, SEPA, and cards. This capability is critical in both the US and UK, where real-time payments significantly reduce response windows⁶.

Risk Scoring and Alert Prioritization

Instead of generating uniform alerts, AI assigns dynamic risk scores using behavioral context and historical outcomes. This approach aligns with regulatory expectations for risk-based monitoring⁷ and significantly improves alert quality.

Anomaly Detection

Machine learning highlights deviations from a customer’s normal behavior, reducing reliance on static thresholds that often generate excessive false positives.

Graph and Network Analysis

Network analytics uncover hidden relationships between accounts, devices, and transactions. This capability is especially effective against fraud rings and mule networks, which are increasingly prevalent in both US and UK fraud cases⁸.

AI Support for AML and KYC

AI also strengthens AML monitoring and KYC automation by:

- Improving customer risk segmentation

- Enhancing sanctions, PEP, and adverse media screening

- Automating periodic reviews and low-risk alert remediation

Why Traditional Systems Fall Short

Despite heavy investment, many financial institutions still operate fraud and AML programs in silos. Separate teams, tools, and datasets lead to duplicated alerts, inconsistent decisions, and missed connections.

Regulators have repeatedly highlighted that fragmented monitoring frameworks increase compliance risk and reduce detection effectiveness⁹. Alerts reviewed in isolation often fail to reveal broader patterns of criminal activity.

The result is:

- High false positive rates

- Long alert remediation cycles

- Increased customer friction during onboarding and payments

Legacy systems were not designed for today’s transaction volumes, data complexity, or regulatory scrutiny.

The AI Paradox: Better Models, More Alerts

AI models are highly effective at identifying nuanced anomalies. However, without orchestration, they can increase alert volumes rather than reduce them.

Industry research shows that institutions deploying machine learning without integrated workflows often experience short-term alert inflation before achieving efficiency gains¹⁰. This reinforces a key lesson:

AI improves detection accuracy, but only unified operating models reduce false positives at scale.

Reducing False Positives Through FRAML Convergence

The Role of Unified Fraud and AML Models

Leading regulators and industry groups increasingly advocate for integrated financial crime risk management, where fraud and AML share data, context, and investigative workflows¹¹.

Sutherland’s FRAML (unified Fraud, risk and AML solution) enables:

- Shared alert pipelines

- Behavioral and transactional data fusion

- Single customer-centric investigations

- Continuous feedback loops for model improvement

This convergence directly improves alert relevance and reduces duplicate investigations.

How KYC Automation Improves Alert Quality

KYC Automation is often viewed as a cost or onboarding efficiency lever. In reality, it is foundational to alert quality.

Poor identity data and outdated risk profiles introduce noise into transaction monitoring systems. According to PwC, institutions with automated, continuous KYC processes experience significantly lower downstream alert volumes and faster investigation times¹².

AI-driven KYC Automation:

- Improves identity verification accuracy

- Continuously updates customer risk profiles

- Eliminates repetitive reviews across fraud and AML teams

The result is fewer unnecessary alerts and more confident decision-making.

Measurable Benefits of AI-Driven FinCrime Detection

When AI is deployed within an integrated operating model, institutions consistently report:

- 30–60% reduction in false positives⁴

- 40–50% reduction in alert handling time¹⁰

- Lower fraud losses and operational costs

- Improved regulatory confidence and audit readiness

Equally important, customer experience improves as legitimate activity flows with fewer interruptions.

Balancing Automation with Human Judgment

AI-driven fraud prevention is not about removing humans from the process. Regulators in both the US and UK emphasize the importance of explainability, governance, and human oversight in AI-supported decision-making⁷.

Successful programs use AI as a decision support layer, enabling investigators to focus on complex, high-risk cases while automation handles routine work.

Why This Matters Now for US and UK Institutions

Fraud tactics are evolving faster than ever. Regulators expect enterprise-wide risk visibility. Customers expect instant, frictionless experiences.

The urgency is no longer about generating more alerts. It is about generating better alerts.

AI-driven FinCrime detection, supported by fraud prevention and KYC automation, is now essential to sustaining trust, compliance, and growth.

Conclusion: From Alert Volume to Alert Value

AI has reshaped the economics of FinCrime detection. Institutions that combine advanced analytics with unified fraud and AML models can reduce false positives, improve alert quality, and strengthen customer trust.

The technology is proven. The regulatory expectations are clear. The need is immediate.

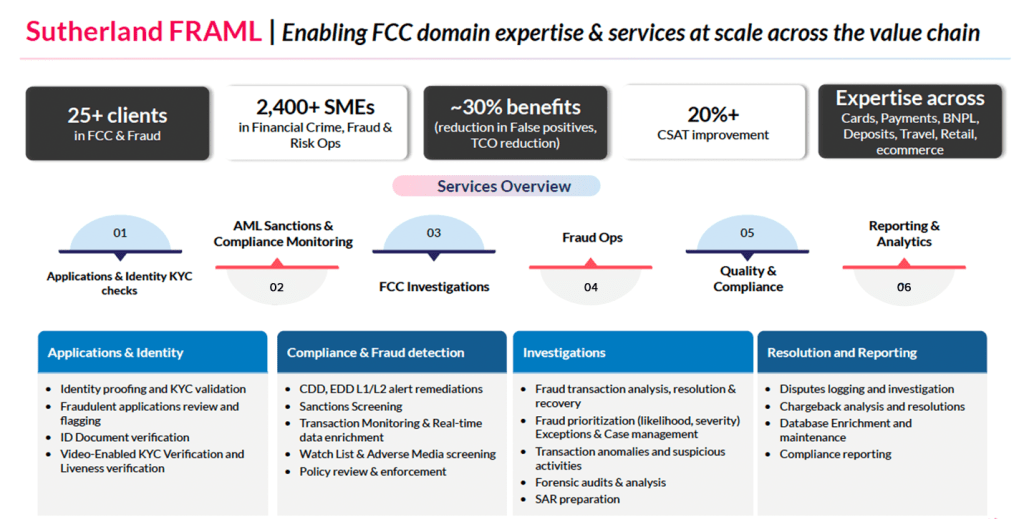

How Sutherland Can Support AI-Driven FinCrime Detection

Sutherland’s AI-powered Financial Crime offering delivers a unified risk, fraud and AML compliance platform that connects customer screening, real-time transaction monitoring, and alert resolution—wrapped in modular managed services.

Backed by 2,400+ domain SMEs (subject matter experts) and AI accelerators like Agentic AI, Sentinel AI, and HelpTree, the solution handles everything from onboarding and watchlist screening to alert triage and SAR (Suspicious Activity Report) filings.

References

¹ U.S. Federal Trade Commission, Consumer Sentinel Network Data Book 2023

² UK Finance, Fraud The Facts 2024

³ Financial Action Task Force (FATF), Risk-Based Approach Guidance

⁴ McKinsey & Company, The Future of Fraud Detection in Banking

⁵ Bank for International Settlements, Sound Practices: implications of fintech developments for banks and bank supervisors

⁶ Federal Reserve, FraudClassifier Model and Real-Time Payments Risk

⁷ UK Financial Conduct Authority, Guidance on the Use of Advanced Analytics in Financial Crime Systems

⁸ Europol, Internet Organised Crime Threat Assessment

⁹ U.S. Department of the Treasury, National Strategy for Combating Financial Crime

¹⁰ Deloitte, Machine Learning and the Evolution of AML Monitoring

¹¹ Wolfsberg Group, Principles for Using Artificial Intelligence and Machine Learning in Financial Crime Compliance

¹² PwC, Global Economic Crime and Fraud Survey